Buying car insurance in India is not only a legal requirement, but also an important financial decision.

Choosing the right insurance can be overwhelming with so many insurers, policy options, and add-ons available. Many people make the mistake of getting the cheapest policy

or blindly following recommendations without understanding what they are paying for. This can lead to inadequate coverage, hidden costs, and unpleasant surprises during claims.

To help you make an informed decision, here are five important factors you should consider before buying car insurance in India.

1. Understand the types of car insurance policies

Before Buying Car Insurance in India,

Before buying insurance, it is important to know the two main types of car insurance policies available in India:

- Third-party liability insurance: This is the minimum legal requirement under the Motor Vehicles Act, of 1988. It covers damage caused to third parties (people, vehicles, or property), but does not cover your car.

In India and many other countries, it is mandatory to have third-party liability insurance or you may face special actions like fines and imprisonment.

- Comprehensive insurance: This includes third-party liability as well as coverage for damage caused to your vehicle due to accidents, theft, natural calamities, fire, etc.

Why it matters: Many people choose third-party insurance because it is cheaper.

However, a comprehensive policy offers better financial protection if your car gets damaged, stolen, or affected by a natural calamity.

Example: Imagine your car gets badly damaged in a flood. A third-party policy will not cover your repair costs, while a comprehensive plan will.

2. Check the insured declared value (IDV) and premium balance

Before Buying Car Insurance in India,

Insured Declared Value (IDV) is the maximum amount your insurer will pay in case of a total loss (theft or irreparable damage). It directly affects your premium:

- Higher IDV means higher premium but better compensation.

- Lower IDV reduces premiums but may leave you underinsured.

Why it matters: Some insurers offer lower premiums by lowering the IDV, but this can be a problem if your car gets stolen or totaled.

Pro tip: Always choose an IDV that reflects the fair market value of your car.

You can check your vehicle’s IDV (Insured Declared Value) by clicking here,

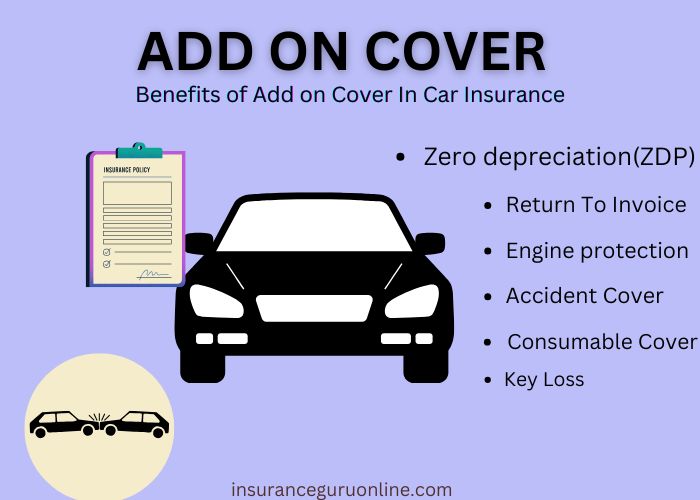

3. Valuable add-on covers for enhanced protection

Before Buying Car Insurance in India,

Add-ons can significantly enhance your coverage, but they also increase the premium. Some useful add-ons include:

- Zero depreciation cover: Ensures full claim settlement without taking depreciation into account.

- Engine protection cover: Covers damage to the engine due to water ingress or oil leakage.

- Roadside assistance: Assists in case of breakdown or emergency.

- NCB protection cover: Keeps your No Claim Bonus intact even after a claim.

Why it matters: Add-ons can provide important protection depending on the usage of your car. For example, if you live in a flood-prone area, engine protection is important.

Example: A friend’s car suffered engine damage due to waterlogging in Mumbai, but since he had an engine protection cover, he did not have to spend heavily on repairs.

4. Compare different insurance companies and their claim settlement ratio

Before Buying Car Insurance in India,

Choosing a reputed insurance company is as important as choosing the right policy. Focus on these:

- Claim Settlement Ratio (CSR): A higher ratio (above 85%) indicates better claim acceptance rates.

- Cashless network garages: More tie-ups mean easier access to cashless repairs.

- Customer service reviews: Check out user reviews to understand real-world experiences.

Why it matters: A low premium means no point if the insurer has a poor claim settlement record or doesn’t have a strong garage network.

Pro tip: Use IRDAI‘s website to verify the insurer’s claim settlement ratio before making a decision.

5. Understand policy exclusions and hidden costs

Every insurance policy has exclusions – situations where claims will not be approved. Common exclusions include:

- Damage caused by driving under the influence of alcohol or drugs.

- Wear and tear, electrical breakdown, or mechanical failures.

- Accidents are caused while using the car for business purposes (if insured for private use).

- Claims filed after policy expiry.

Why it matters: Many people believe insurance covers everything, but later face claim rejections.

Example: A driver in Delhi met with an accident while driving without a valid license. His claim was rejected because it fell under a policy exclusion.

FAQ section

Q1. Is third-party insurance enough for my car?

If you have an old car with low market value, third-party insurance might be sufficient. However, for newer cars, comprehensive insurance is recommended for better protection.

Q2. How is the car insurance premium calculated?

Premiums depend on factors like the car’s IDV, make and model, engine capacity, location, and selected add-ons.

Q3. Can I transfer my No Claim Bonus (NCB) to a new car?

Yes, NCB is linked to the policyholder, not the car. You can transfer it when you buy a new car.

Q4. What happens if I miss renewing my car insurance on time?

Your policy will lapse, and you will lose benefits like NCB. Additionally, you cannot legally drive the car without insurance.

Q5. Can I switch insurers if I find a better deal?

Yes, you can switch insurers at the time of renewal. Make sure to transfer your NCB and compare policies carefully before switching.

Conclusion

Buying car insurance is more than just fulfilling a legal requirement—it’s about ensuring financial security.

By understanding the policy type, IDV, add-ons, claim settlement history, and exclusions, you can choose a policy that offers real protection rather than just being the cheapest option.

Before finalizing your policy, take the time to compare different plans, read the fine print, and ensure it suits your needs. Investing in the right insurance today can save you from unexpected expenses and stress in the future.

Final tip: Use online comparison tools and consult professionals when needed. Making an informed choice can make a big difference! Check out the latest insurance information and other best insurance information.